what is gross income?

Gross income means – all income derived from whatever source including but is not limited to the following:

1.Compensation for services in whatever form paid

2.Gross income from the conduct of trade or business or practice of profession

3.Gains derived from dealings in property

4.Interests

5.Rents

6.Royalties

7.Dividends

8.Annuities

9.Prizes and winnings

10.Pensions

11.Partner’s distributive share from the net income of the GPP

1.Compensation for services in whatever form paid

2.Gross income from the conduct of trade or business or practice of profession

3.Gains derived from dealings in property

4.Interests

5.Rents

6.Royalties

7.Dividends

8.Annuities

9.Prizes and winnings

10.Pensions

11.Partner’s distributive share from the net income of the GPP

what are exclusion from gross income?

1.Proceeds of life insurance paid to the beneficiary upon death of the insured

2.Amount received by the insured as a return of premium

3.Gifts, bequests and devises

4.Compensation for injuries or sickness

5.Income exempt under treaty

6.Retirement benefits, pensions, gratuities

7.Miscellaneous items

a .Income derived by foreign government

b. Income derived by the government or its political subdivisions

c. Prizes and awards – in recognition of religious, charitable, scientific, educational,

artistic, literary or civic achievement subject to two conditions

d. Prizes and awards in sports competition

e.13th month pay and other benefits

f. GSIS, SSS, Medicare, Pag-ibig contributions and Union dues

g. Gains from the sale of bonds, debentures or other certificate of indebtedness with

maturity of more than 5 years

h .Gains from redemption of shares in mutual fund

2.Amount received by the insured as a return of premium

3.Gifts, bequests and devises

4.Compensation for injuries or sickness

5.Income exempt under treaty

6.Retirement benefits, pensions, gratuities

7.Miscellaneous items

a .Income derived by foreign government

b. Income derived by the government or its political subdivisions

c. Prizes and awards – in recognition of religious, charitable, scientific, educational,

artistic, literary or civic achievement subject to two conditions

d. Prizes and awards in sports competition

e.13th month pay and other benefits

f. GSIS, SSS, Medicare, Pag-ibig contributions and Union dues

g. Gains from the sale of bonds, debentures or other certificate of indebtedness with

maturity of more than 5 years

h .Gains from redemption of shares in mutual fund

DEDUCTIONS FROM GROSS INCOME

REQUISITE

1.Ordinary

2.Necessary

3.Incurred in taxable year

4.Attributable to the development, management or operation of the business or trade

5.Reasonable

6.Withholding tax is paid (Rev. Reg. 6-2018)

7.Proof

ITEMIZED:

1.Expenses

I. Salaries and wages

ii. Transportation and travel

iii .Rental and other payments

iv. Entertainment, amusement, recreation*

2.Interest*

3.Losses

4.Taxes

5.Bad debts

6.Depreciation

7.Depletion

8.Charitable and Other Contribution (w /limitation)

9.Pension Trust

1.Ordinary

2.Necessary

3.Incurred in taxable year

4.Attributable to the development, management or operation of the business or trade

5.Reasonable

6.Withholding tax is paid (Rev. Reg. 6-2018)

7.Proof

ITEMIZED:

1.Expenses

I. Salaries and wages

ii. Transportation and travel

iii .Rental and other payments

iv. Entertainment, amusement, recreation*

2.Interest*

3.Losses

4.Taxes

5.Bad debts

6.Depreciation

7.Depletion

8.Charitable and Other Contribution (w /limitation)

9.Pension Trust

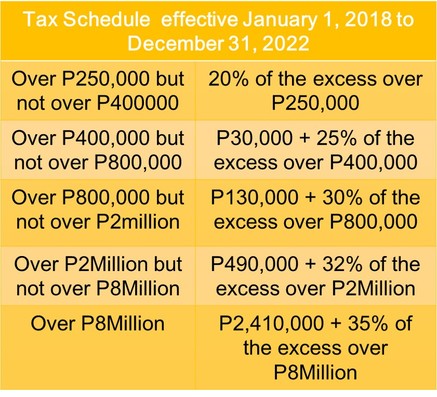

annual tax table

optional standard deductions

Individual Taxpayer - 40% of Gross Sales/Receipts

Non-Individual Taxpayer - 40% of Gross Income

EXAMPLE:

Individual Corporation

Gross sales/receipts 1,000,000 1,000,000

Less: Cost 0.00 500,000

Gross Income (profit) 1,000,000 500,000

Less: OSD 400,000 200,000

Taxable Income 600,000 300,000

Not applicable to:

• Non-resident alien engaged in trade

• Exempt Taxpayers

• Preferential Rate Taxpayers

• Compensation Income Earners

• Taxpayers who chose 8% optional tax rate

Note:

Non-Individual Taxpayer - 40% of Gross Income

EXAMPLE:

Individual Corporation

Gross sales/receipts 1,000,000 1,000,000

Less: Cost 0.00 500,000

Gross Income (profit) 1,000,000 500,000

Less: OSD 400,000 200,000

Taxable Income 600,000 300,000

Not applicable to:

• Non-resident alien engaged in trade

• Exempt Taxpayers

• Preferential Rate Taxpayers

• Compensation Income Earners

• Taxpayers who chose 8% optional tax rate

Note:

- Choose Method of Deduction on 1st quarterly income tax return or initial return

- Irrevocable for the year

- GPP allowed to claim OSD

8% Optional Income Tax

• In lieu of income tax and percentage tax

• Basis is actual gross sales/receipts and other non-operating income

• Signify on 1st quarterly income tax return or initial return

• Irrevocable for the taxable year

• If no intention was made, deemed graduated tax rate

• Audited financial statements is not a requirement

• Bookkeeping and Invoicing Rules apply

Not applicable to:

• VAT-registered Taxpayers

• Taxpayers subject to Other Percentage Taxes

• Partners of a GPP

• Taxpayers who opted for OSD

• Taxpayers whose gross sales and non-operating income exceeded the

VAT threshold

• Taxpayers who did not signify their intent to be taxed at 8%

• Basis is actual gross sales/receipts and other non-operating income

• Signify on 1st quarterly income tax return or initial return

• Irrevocable for the taxable year

• If no intention was made, deemed graduated tax rate

• Audited financial statements is not a requirement

• Bookkeeping and Invoicing Rules apply

Not applicable to:

• VAT-registered Taxpayers

• Taxpayers subject to Other Percentage Taxes

• Partners of a GPP

• Taxpayers who opted for OSD

• Taxpayers whose gross sales and non-operating income exceeded the

VAT threshold

• Taxpayers who did not signify their intent to be taxed at 8%

RSS Feed

RSS Feed